Top Cashfree Competitors for International Payments in India (2026)

Why you’re here

Cashfree makes it easy to manage both domestic and international flows in one place. As export volumes grow, some teams explore adjacent options, not because Cashfree “doesn’t work,” but to see which platform best matches their ticket sizes, settlement needs, FX preferences, and compliance workflow.

Cashfree, in brief (cross-border)

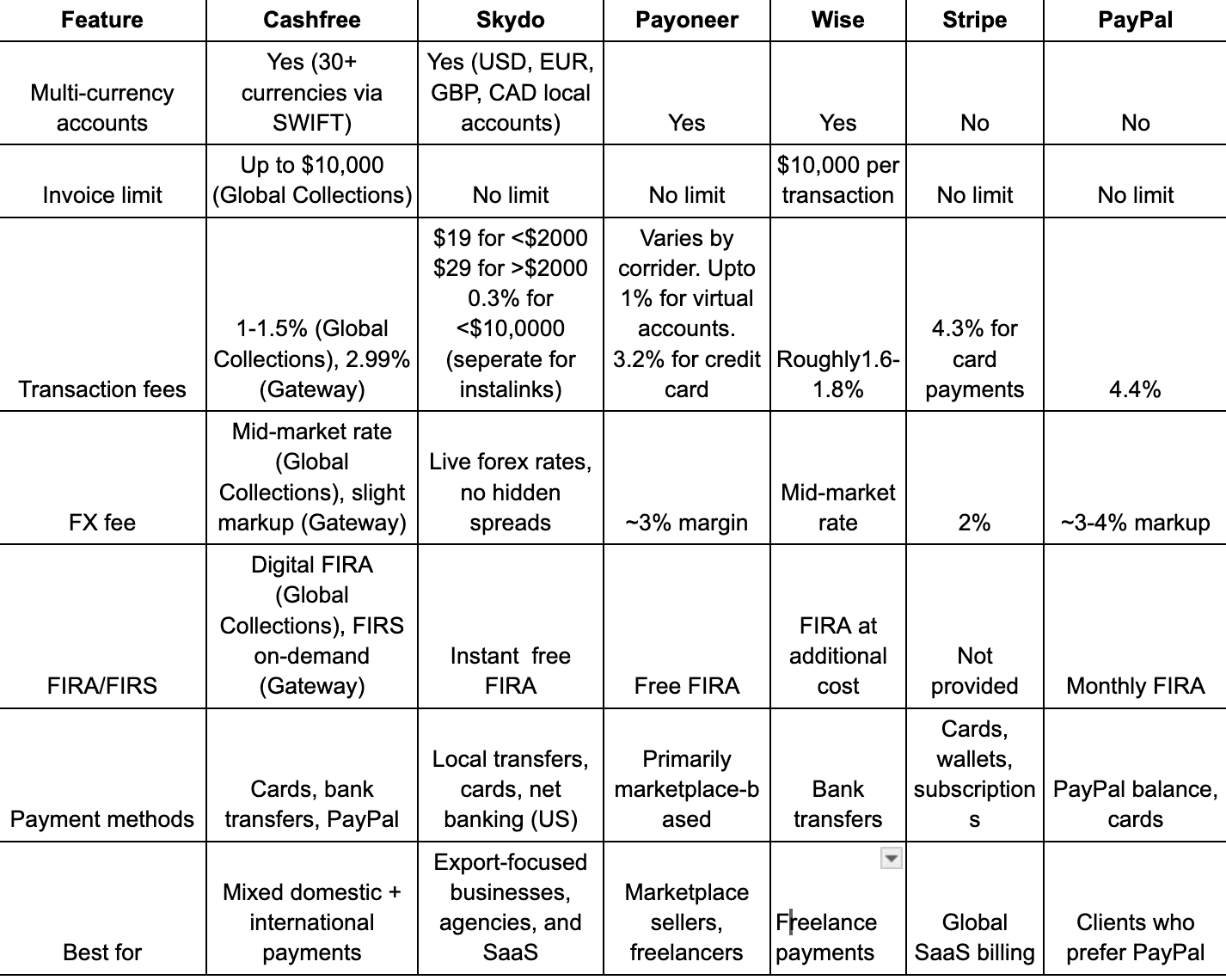

- Global Collections Account: Virtual accounts in major currencies; clients pay via local rails or SWIFT. INR settlement follows. Per-invoice eligibility up to $10,000 with exporter documentation.

- International Payment Gateway: Accept international cards/APMs with INR settlement.

- Compliance docs: You get FIRS(summary reports) with the payment gateway, and per-payment FIRAs with global collection accountnts.

- Pricing snapshot: International card fees are typically 2.99%, with time-bound promos available. For its payment gateway, Cashfree advertises "best rates" for conversion, meaning there's possibly a small markup added.

Global Collections pricing varies by corridor/volume but typically ranges between 1%-1.6% and it also offers live forex rate while conversion.

Think of Cashfree as a generalist payments stack that also supports export collections.

When teams look for Cashfree alternatives

Three shifts usually trigger the search:

- Predictable FX and fees. Once you start checking margins at a per-invoice level, even a tiny forex markup adds up substantially. Exporters prefer mid-market (0% markup) + a transparent fee so they can price with confidence.

- Settlement speed: 24-hour settlement often becomes crucial for exporters and businesses handling multiple vendor payments and payroll

- Documentation by default: Per Payment FIRA for every transaction, is not only crucial for compliance but also for claiming GST refunds

With that lens, here are the leading alternatives to Cashfree and where each one fits.

Skydo: Export-first collections (freelancers, agencies, SaaS, exporters)

If your revenue is primarily from overseas clients, Skydo is purpose-built for that motion.

- You get global bank accounts in your business’s name (USD/EUR/GBP/CAD), so clients pay you like a local vendor using familiar rails.

- For US buyers, there’s also InstaLinks to pay by card or ACH debit.

Three things stand out for export teams:

- Two things stand out for export teams: mid-market FX with 0% markup and flat, transparent fees (e.g., $19/$29/0.3% + GST; InstaLinks 5% card, 2% ACH).

- Every payment comes with an instant FIRA, and if you sell on Amazon Global, you can get eBRC as well.

- Settlements are quick, often within 24 hours, so your cash flow doesn’t stall.

Why pick Skydo over other Cashfree competitors? Because it removes guesswork where exporters feel it the most: FX clarity, compliance artefacts, and payout speed.

Payoneer: Marketplace-native (Amazon Global, Upwork, Fiverr)

If most of your receivables come from marketplaces, Payoneer is familiar—and for good reason. You can receive in multiple currencies, withdraw to your Indian account, and keep your accounting straightforward. Payoneer also offer free FIRA for every payment.

Fees vary by route and volume. For virtual account transfers, fees can be up to 1%, while credit card payments carry a 3.2% fee+ a small fixed fee. There's also a 3% conversion fee while converting the amount to INR.

Pick Payoneer if your primary motivation is “get paid from marketplaces reliably” and you value minimal setup over granular control of each corridor.

Wise Business: Transparent FX for lighter volumes

Wise is known for its mid-market FX and its super intuitive UI. If your cross-border volume is under USD 10k, Wise’s multi-currency accounts and predictable conversion method feel refreshingly simple.

Wise supports up to USD 10k/invoice and also offers fira for every payment, albeit at an additional cost of USD 2.50

As mentioned, it offers a midmarket rate without any markup and its fee ranges mostly between 1.6-1.8%.

Choose Wise if you prize transparency and ease, and your current scale doesn’t demand advanced export workflows.

Stripe: Global SaaS billing (India availability varies)

For teams with a strong subscription or recurring billing motion, Stripe is a developer’s favourite: flexible pricing models, solid APIs, and battle-tested tooling across many currencies. However, here are the things you need to know

- Sripe is currently 'invite-only" in India. You need to request access, and there's no definite timeline on when it will be granted

- Stripe doesn't offer FIRA for international payments

- Stripe's cumulative fees, including transaction fees and currency conversion, can be up to 6.2%

Choose Stripe when your product is subscription-led and engineering flexibility matters more than out-of-the-box export ops.

PayPal: Familiarity that can lift conversion

Sometimes the fastest way to get paid is to meet the buyer where they already are. PayPal is globally recognised, often improving first-time conversion.

On the flip side, total cost (cross-border + conversion) can be up 8% higher than bank-rail options. It offers a monthly digital FIRA that is available by the 15th of the next month

Choose PayPal when buyer preference is the deciding factor and you want instant recognizability.

Comparison at a glance

Cashfree vs competitors: how to actually choose

- Invoice-led export collections (freelancers/agencies/SaaS): Skydo, export-first rails, mid-market FX (0% markup), flat fees, instant FIRA, fast INR (<24h); US InstaLinks for card/ACH.

- Mixed domestic + international with checkout/APMs in one stack: Cashfree, unified gateway + collections, cards/APMs, INR settlement; consolidated e-FIRS on gateway and FIRA on global collection accounts

- Marketplace-heavy income (Amazon Global, Upwork, Fiverr): Payoneer, native marketplace flows, multi-currency receiving, straightforward withdrawals.

- Smaller payments with transparent FX: Wise, mid-market rate, simple setup; good for lighter volumes and clarity on conversion.

- Subscriptions/recurring SaaS billing (developer-driven): Stripe, robust billing/subscriptions, global acceptance (India availability varies).

- Buyer insists on PayPal, unsure of new platforms: PayPal, Global familiarity and credibility

Bottom line

If you’re happy with a single, generalist stack, Cashfree does the job, especially when you need domestic + international + gateway in one place. I

If you’re running an export-led operation and want mid-market FX, flat fees, faster INR, and per-payment FIRA by default, shortlisting Skydo is a smart next step.

Does Cashfree support international payments?

Yes. Cashfree lets Indian businesses receive foreign payments through its Global Collections Account and international payment gateway, both settling in INR.

What’s the per-invoice limit for Cashfree’s Global Collections?

hich Cashfree alternative offers mid-market FX and instant FIRA?