What Is an Intermediary Bank? Meaning, Details, and Hidden Costs

If you’ve ever received an international wire transfer and noticed the amount was less than expected, an intermediary bank was likely involved.

But what is an intermediary bank, and why does it take a cut from your payment?

Let’s break it down.

Intermediary Bank Meaning (Simple Explanation)

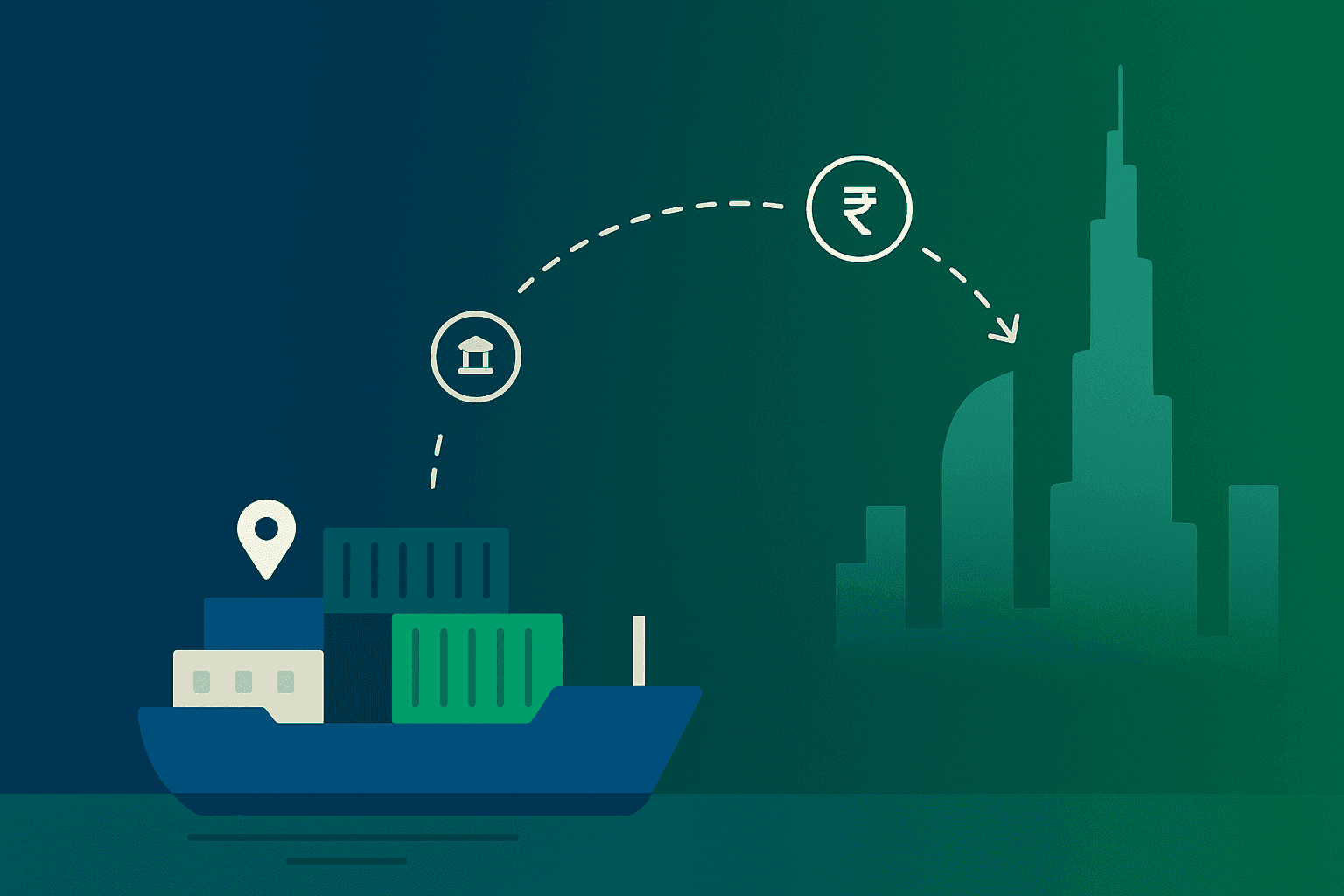

An intermediary bank is a third-party bank that helps route international payments when the sender’s and receiver’s banks don’t have a direct relationship.

For example, if a client in the US pays you in USD, and your Indian bank doesn’t have a direct relationship with the US bank, the payment travels through one or more intermediary banks before reaching your account.

These banks work behind the scenes, which means you don’t usually know when they’re involved. But they can silently eat into your earnings by deducting hidden charges during the transfer.

When Do Intermediary Banks Get Involved?

Intermediary banks are used when international transfers are made through the SWIFT network, especially in the following situations:

1. No Direct Banking Relationship

If your Indian bank doesn’t maintain a Nostro account (foreign currency account) with the sender’s bank, intermediary banks are used to bridge the gap.

2. No USD Clearing Partner

Many Indian banks don’t have a direct USD clearing arrangement. The payment is routed through intermediary banks that can handle USD transactions.

3. Currency Conversion Needs Routing

If your client is paying in a currency their bank doesn’t directly support (like Swiss Franc to INR), the bank uses an intermediary to settle the payment.

Intermediary Bank Charges: How They Eat Into Your Payments

Here’s the tricky part: intermediary bank fees are deducted silently.

- Typical deduction: $10–$30 per intermediary

- No invoice or alert: These fees don’t appear on your or your client’s bank statement

- Multiple intermediaries = multiple deductions

💡 Example: Your client sends $1,000. After two intermediary banks take $14 each, you receive only $972, with no breakdown to show why.

Why It Matters for Freelancers and Exporters

Intermediary bank deductions may seem small, but they add up:

- Lose ₹2,000/month if you receive just 10 payments with a $25 cut per transfer

- Lose 3–4% of your revenue if you add hidden FX markups to intermediary bank charges

- Cash flow delays: Each intermediary can add 1–2 days to your settlement time

- Accounting headaches: Reconciliation becomes harder when payments don’t match invoice amounts

Can You Avoid Intermediary Bank Charges?

You can’t skip intermediary banks every time, but here’s how to reduce or eliminate the charges:

❌ Avoid

- Banks that don’t disclose intermediary fees. If your bank isn’t transparent, switch to a provider that is.

- Personal savings accounts for receiving business payments .They often trigger more intermediaries. Use a business current account instead.

✅ Prefer

- Banks/platforms with direct USD/ foreign currency clearing

This reduces or removes intermediary bank involvement.

- Platforms that show the remitted vs. received amount

Transparent platforms help you track every dollar.

Intermediary Bank vs Beneficiary Bank: Quick Note

Your beneficiary bank is the one that receives the funds on your behalf. An intermediary bank is just a middleman that helps route the funds, and quietly charges a fee along the way.

How Skydo Helps You Avoid Intermediary Bank Fees

Skydo offers a smarter, cleaner alternative to traditional SWIFT transfers.

✅ virtual bank accounts in the US, UK, EU, Canada, and Singapore.

These accounts are powered by Skydo’s partnerships with major global banks like Community Federal Savings Bank (US), Barclays (EU), DBS (Singapore), etc.

✅ No intermediary banks involved

Payments are collected locally and credited to your Indian account, fast and fee-free.

✅ Transparent fee structure

Flat fee, no hidden charges, no fx markup , conversion happens at the live mid-market rate.

✅ Fully compliant

Skydo is authorised by the RBI under the Payment Aggregator Cross Border (PA-CB) framework and follows all required regulations.

Skydo vs Traditional Banks (At a Glance)

| Fee Component | Traditional Banks | Skydo |

| Intermediary Bank Fees | $10–$50 | $0 |

| FX Markup | 2%-5% | 0% |

| Wire Transfer | Fee$30–$45 | $0 |

| FIRA Charges | INR 200-500 | INR 0 |

| Settlement Time | 1-5 business days | 24-48 hours |

Final Word

Intermediary banks are often invisible, but they can cost you more than you think, in both money and time.

Skydo helps you bypass them entirely, giving you faster, cheaper, and transparent global payments.

👉 Ready to stop losing money to invisible fees?

Sign up for a free demo with Skydo today

What is an intermediary bank?

An intermediary bank is a third-party bank that helps process international wire transfers when the sender’s and receiver’s banks don’t have a direct relationship. It acts as a bridge to route the payment through the SWIFT network.

Why do intermediary banks charge fees?

How do I know if an intermediary bank is involved?