What Is SWIFT MT103? Format, Fields, and How to Get One

TL;DR - Summary

- What is MT103: - An MT103 is a standardized SWIFT message that confirms an international transfer was sent.

- What does an MT103 contain: - An MT103 SWIFT message contains details on sender & recipient, amount & currency, routing banks, and more.

- Recent update on SWIFT MT103: - MT103 was replaced by PACS.008 in November 2025, though some banks are still transitioning.

What Is a SWIFT MT103 Message?

An MT103 is the standardized SWIFT message for international wire transfers. Every time money moves across borders through the SWIFT network, an MT103 is generated at the sending bank to record the transfer. It is not the money itself, but it is the structured message that instructs and records the transfer, carrying all the key details of the transaction. This document becomes highly useful to track a payment, resolve disputes over a short amount or to reconcile your records.

What Information Does a SWIFT MT103 Contain?

An MT103 contains the following information:

- Sender and recipient details: the name, account number, and bank of whoever initiated and is receiving the transfer

- Transaction details: the amount, currency, value date (the date the funds settle between banks), and the unique transaction reference number

- Routing information: any intermediary or correspondent banks the payment passed through on its way to the beneficiary

- Charge details: who is paying the transfer fees, the sender, the recipient, or split between both

Each of these sits in a specific field tagged with a code like :20: or :32A:. Once you know what each tag means, the document becomes easy to read.

Why Do We Need SWIFT MT103 in International Payments?

The MT103 is useful in four situations: proving a payment was sent, tracking a delayed payment, resolving a dispute over a short amount, and reconciling your records.

Tracking delayed payments: Every MT103 carries a UETR, a 36-character tracking code mandatory for all SWIFT payments. Share this with your bank and they can trace exactly where the payment is in the SWIFT network, provided all banks in the chain support SWIFT gpi.

Proof of payment: The MT103 proves whether a SWIFT wire was actually sent. It shows the date, amount, reference number, and which banks were involved. If a sender claims they paid and you have not received anything, this is the document that settles it.

Resolving payment disputes: Field 71A shows the charge arrangement between the sender and the receiver. OUR means the sender paid all fees and you should receive the full amount. SHA means charges are to be shared by the sender and the receiver. BEN means all charges fall on you. If you received less than invoiced, Field 71A tells you whether the deduction was due to the charge arrangement.

Reconciliation: The MT103 shows the original amount sent and the final amount settled between banks. If your client sent $5,000 but only $4,960 reached you, the MT103 shows the fees deducted along the way. If the payment involved a currency conversion, it may also show the exchange rate used.

Imagine you’ve paid an overseas supplier, but they claim the funds haven’t arrived. You check with your bank, and they confirm the SWIFT transfer was sent – now you’re stuck in the middle, unsure who to believe. This is where the MT103 comes in. By obtaining the MT103 document, you get a detailed record of the payment showing when and where the money was sent, and through which banks.

You can forward this to the beneficiary as proof of payment, and your bank can use the reference information in the MT103 to help trace the payment’s path and find any bottlenecks in the process. Often, just providing the MT103 to the beneficiary’s bank is enough for them to locate a pending credit in their system.

SWIFT MT103 Format and Fields

An MT103 contains numbered fields, each identified by a tag that begins with a colon. The fields appear in a standard sequence and each one carries a specific, consistent meaning regardless of which bank issued it.

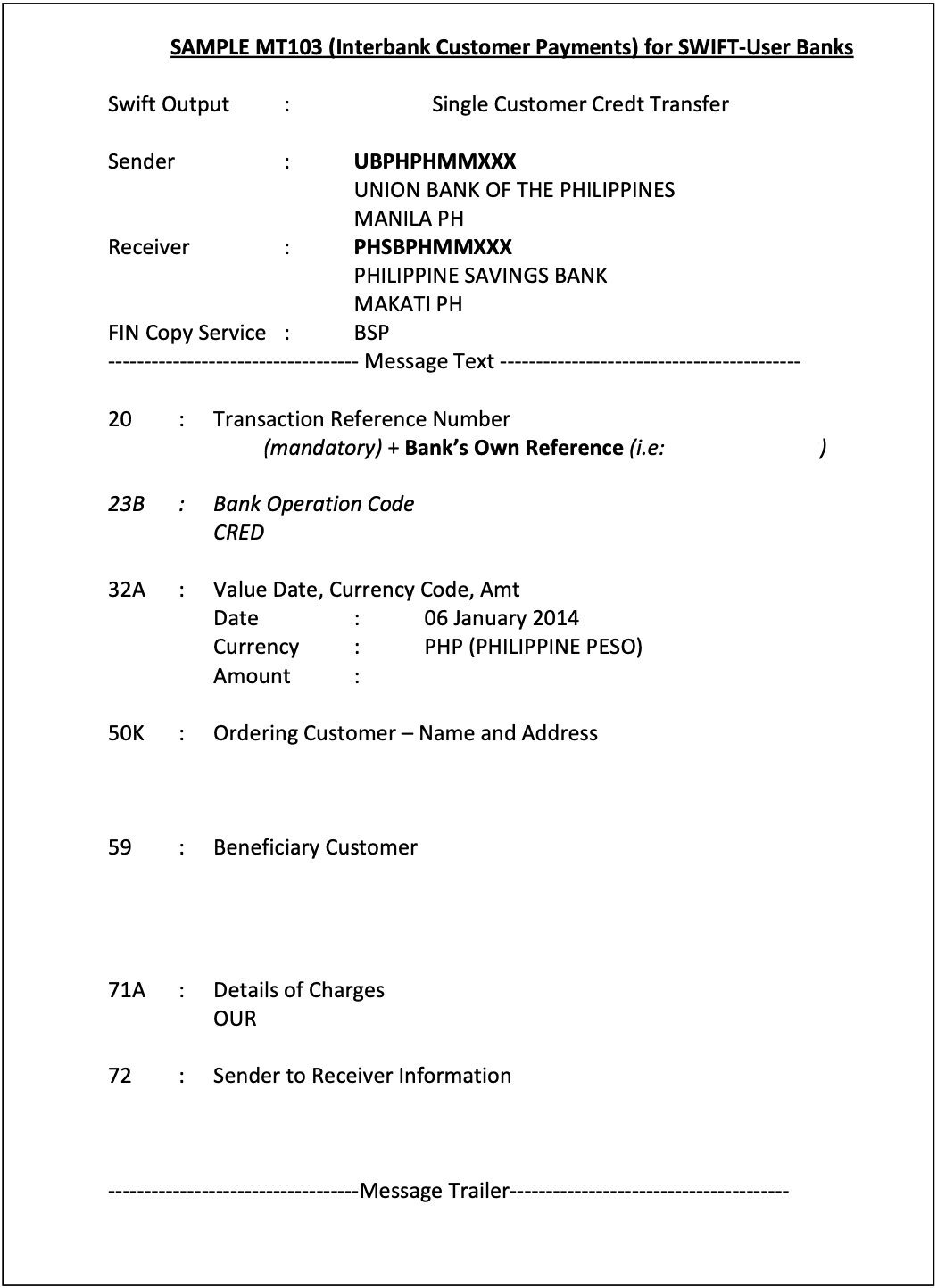

Below is what a sample SWIFT MT103 looks like:

SWIFT MT103 Sample

SWIFT MT103 SampleHere are some of the most essential fields you need to know to understand the SWIFT MT103 document.

| Tag | Field Name | What It Contains | Required? | What to Check |

|---|---|---|---|---|

| Tag:20: | NameTransaction Reference | ContainsUnique ID assigned by sending bank | RequiredYes | CheckSave this for tracing the payment |

| Tag:23B: | NameBank Operation Code | ContainsUsually CRED (credit transfer) | RequiredYes | CheckConfirms it is a standard transfer |

| Tag:32A: | NameDate / Currency / Amount | ContainsValue date, currency code, settled amount | RequiredYes | CheckCompare with your invoice amount |

| Tag:50A: | NameOrdering Customer | ContainsSender's name, account, address | RequiredYes | CheckConfirms who paid you |

| Tag:59: | NameBeneficiary Customer | ContainsRecipient's name, account or IBAN | RequiredYes | CheckVerify your details are correct |

| Tag:71A: | NameDetails of Charges | ContainsOUR / BEN / SHA — who pays fees | RequiredYes | CheckExplains any fee deductions |

| Tag:56A: | NameIntermediary Bank | ContainsBIC of intermediary bank if used | RequiredNo | CheckHelps trace where fees were deducted |

| Tag:70: | NameRemittance Information | ContainsInvoice number, payment purpose | RequiredNo | CheckHelps you match payments to invoices |

| Tag:72: | NameSender to Receiver Info | ContainsAdditional instructions or notes | RequiredNo | CheckRead for any sender notes |

Every MT103 has specific field tags as outlined above, and learning to read them can be useful. You don’t need to memorise every code, but knowing the key fields helps.

For most users, the critical things to check on an MT103 copy are:

- The transaction reference number (to track it)

- The dates and amount (to confirm timing and amount sent),

- The beneficiary details (to ensure the money was directed to the correct account), and

- The charges field (to see if any fees were taken out).

Mandatory vs. Optional Fields in SWIFT MT103 Format

Some fields appear on every MT103, while others are optional or used only in certain cases. We have covered the common mandatory fields (like 20, 32A, 50, 59, 71A, etc.) here so that you can easily skim through them to get an undersatnding

- Time Indication (Tag :13C:) – Timestamps for various processing events (e.g. time of sending and receiving).

- Transaction Type Code (Tag :26T:) – Indicates the purpose of the transaction (salary, trade payment, etc.) if provided.

- Exchange Rate (Tag :36:) – If currency conversion was involved, the rate can be indicated here.

- Sender to Receiver Info (Tag :72:) – Free-format text for any additional instructions from the sending bank to the receiving bank (often used for things like regulatory info or special notes).

These optional tags might not appear on every MT103, but they offer flexibility to include extra details when needed. For example, a Tag 72 might carry a note like “/INS/ intermediary bank fees to be charged to sender,” or other instructions that don’t fit in the standard fields.

How To Get a SWIFT MT103?

The MT103 is generated and held by the sending bank. As the receiver, the only way to get it is to ask the sender to request a copy from their bank and share it with you.

Here is a step-by-step process on how you can get a copy of the SWIFT MT103.

How to get an MT103

You ask the sender

Request the MT103 from your client who made the payment

Sender contacts their bank

Via customer service, branch visit, or online portal. Provides transaction reference, amount, date, and recipient details

Bank processes the request

Cost: $20 to $50 | Time: a few hours to 2 business days

Sender receives MT103 as PDF and forwards it to you

Use it to trace the payment, resolve disputes, or reconcile records

In some countries, the MT103 might be referred to by a different name. For example, in India, some banks might call it a “SWIFT Advice” or “SWIFT Copy” instead of using the code “MT103” – but it’s the same document. Don’t be confused by terminology; just clearly ask for proof of the SWIFT transfer or a SWIFT payment confirmation document if the bank seems unsure.

When should you request an MT103?

Since your client's bank may charge them for obtaining an MT103, ask for an MT103 only when you actually need it.

The situations where it's worth asking:

- A payment is delayed or you suspect it's stuck with an intermediary bank.

- You need it for compliance documentation, audits, or tax records.

- Your bank is asking for proof of the inward remittance to process your FIRC or resolve a query.

If the payment landed in your account without issues, you don't need it. Your bank's credit advice or account statement is sufficient for most purposes.

Who Can Request an MT103?

Only the sender can request an MT103, since it is generated by the sending bank and released only to their account holder. If you are the recipient waiting on proof of payment, you cannot get it directly from the bank. You need to ask your client to request it from their bank and forward it to you.

How To Track a SWIFT Payment Using MT103?

When a payment is delayed, you have two ways to trace it depending on what you have.

Using Field 20: Ask the sender to contact their bank and request a payment status update using the Field 20 transaction reference. The sending bank can query the SWIFT system and tell them where the payment is.

Using the UETR: The UETR is a 36-character code mandatory on all SWIFT payments since 2018. Unlike Field 20, it travels unchanged across every bank in the chain. The sender shares the UETR with you, and you can give it to your own bank's forex desk and ask them to run a gpi trace. If your bank supports SWIFT gpi, they can see the real-time status of the payment, whether it is still with the sending bank, in transit at a correspondent bank, or held at your bank pending compliance checks.

If the payment has been stuck for more than three business days after the value date in Field 32A, escalate formally using both references.

SWIFT gpi stands for Global Payments Innovation. It is SWIFT's tracking layer that gives every participating bank real-time visibility into where a payment is.

MT103 vs. SWIFT gpi: What’s the Difference?

It’s worth noting that SWIFT gpi is a newer initiative to modernise cross-border payments. MT103 is a message (a document) confirming the payment was sent. SWIFT gpi, on the other hand, is a tracking system/network upgrade that allows end-to-end visibility in real time.If we use a courier analogy, MT103 is like your shipment receipt and tracking number, whereas SWIFT gpi is the online tracking system you plug that number into, to see exactly where the package (payment) is.

Many banks now embed the UETR from SWIFT gpi into the MT103 message itself, effectively linking the two. The table below summarises it:

| Feature | SWIFT gpi | MT103 |

|---|---|---|

| What it is | Real-time payment tracking across banks with live status updates | Confirmation of payment sent, a receipt with full transaction details |

| When it's generated | Throughout the payment journey, with continuous updates | At the time the payment is initiated, as a one-time message |

| Includes tracking info | Yes, with live updates like "in transit" or "credited," often via UETR | Contains reference numbers (including UETR) and all details, which can be used to trace manually |

| User access | Banks (and sometimes customers, through portals) can check live status | Customers use it as proof and can hand it to banks to trace a payment manually |

Is MT103 Being Replaced?

As of November 22, 2025, SWIFT replaced MT103 with PACS.008 on FINplus, its upgraded messaging network that supports the new ISO 20022 standard. Banks that have not yet migrated can still send MT103 messages, which SWIFT automatically converts to PACS.008 before delivery to the receiving bank. This is why you may still encounter MT103-formatted documents depending on which bank the sender uses.

What Is PACS.008?

PACS.008 is the ISO 20022 replacement for MT103. It carries the same core information, sender, recipient, amount, currency, routing, but uses a more structured data format that supports richer remittance details and handles Indian names and addresses correctly, which the old MT103 character set could not always do.

What Does This Mean for Indian Freelancers and Exporters?

Nothing changes practically. When you ask the sender to request a payment confirmation from their bank and share it with you, that document may now be formatted as PACS.008 rather than MT103. It serves the same purpose. When someone says "ask for the MT103," what they mean going forward is "ask for the SWIFT payment confirmation document."

MT103 vs MT202: Which One Do You Need?

When an international payment moves through the SWIFT network, two different messages are generated: the MT103, which carries the customer transaction details, and the MT202, which handles the settlement between banks behind the scenes. Both are part of the same payment, but they serve completely different purposes and are meant for completely different audiences.

MT103 is the customer transfer message. It carries all the details of the actual transaction: who sent the money, who receives it, the amount, and the purpose. This is the document you or your client would request as proof of payment.

MT202 is a bank-to-bank message. Banks use it to settle funds between themselves, often to cover an MT103 that's already been sent. It contains no customer details whatsoever, and it's never something you need to request or track.

For exporters and freelancers, the rule is simple: if someone asks for proof of an international payment, the document they want is the MT103. The MT202 exists, but it operates entirely within the banking system. You will never see it, and you will never need it.

How Virtual Account Platforms Eliminate the Need for MT103

When Indian exporters and freelancers use virtual usd account platforms like Skydo, the need for MT103 in routine situations largely disappears. This is because virtual accounts receive payments through local rails, ACH in the US, SEPA in Europe, Faster Payments in the UK, rather than SWIFT. When a sender pays via local rails into a virtual account, no SWIFT message is generated, which means no MT103, but also no intermediary bank fees, no multi-day delays, and no need to chase documentation.

The platform itself provides the payment confirmation, generates your e-FIRA automatically, and gives you a clean record for compliance purposes. The SWIFT-and-MT103 process only becomes relevant when a sender insists on a traditional wire transfer.

Most of your international payments do not need to go through SWIFT at all. Skydo gives you local USD, GBP, EUR and SGD accounts so your clients pay locally and you receive faster, with zero intermediary deductions. Get your virtual account

Is MT103 still used in 2026, or has it been replaced by PACS.008?

MT103 was replaced by PACS.008 on SWIFT's FINplus network as of November 22, 2025. However, banks that have not yet migrated can still send MT103 messages, which SWIFT converts to PACS.008 automatically. So depending on which bank the sender uses, you may still encounter MT103-formatted documents.

Can I get an MT103 if I am the receiver, not the sender?

What is UETR and how do I use it to track my payment?

Is MT103 the same as a payment confirmation or bank advice?

How Much Do Banks Charge for an MT103 Copy?